The federal government just rolled out a massive new savings experiment, and honestly, most parents are missing the fine print.

On July 4, 2026, President Trump officially launched Trump Accounts, a brand-new tax-advantaged investment vehicle aimed at every American kid under 18. Created through the One Big Beautiful Bill Act (OBBBA), the Treasury Department designed these accounts to act like a starter retirement fund for children. The White House even hosted an Oval Office event where Trump rang the opening bells for the NYSE and Nasdaq to kick things off.

But if you think this is just another 529 college fund or a standard custodial account, you're mistaken. There are strict guardrails, free money on the table, and some massive traps if you don't know what you're doing. Let's look at exactly how Trump Accounts work and how to handle them.

The Reality Behind Trump Accounts for Kids Under 18

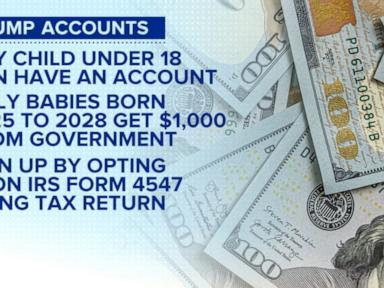

If you have a child with a valid Social Security number who won't turn 18 before the end of the year, they qualify. The absolute biggest headline here is the free cash. The government established a pilot program offering a one-time $1,000 "seed" deposit for eligible U.S. citizens born between January 1, 2025, and December 31, 2028.

But what if your kid was born before 2025? They don't get the federal grand. However, corporate and charitable donors are stepping in. For example, the Michael & Susan Dell Foundation committed $6.25 billion to fund automatic $250 deposits for up to 25 million children aged 10 or younger who live in qualifying lower-income ZIP codes.

Once the account is live, anyone can contribute: you, grandparents, friends, or employers. The annual contribution cap is $5,000 per child, which will start adjusting for inflation in 2028. If your employer has a qualifying contribution program, they can pitch in up to $2,500 per year, though that money counts toward your child's overall $5,000 annual limit.

Where the Money Actually Goes

You can't just open a Trump Account and day-trade tech stocks or buy crypto. The government locked these accounts down during what they call the growth period—which lasts until December 31 of the year before your kid turns 18.

During this childhood phase, regulations restrict all investments to low-cost U.S. equity index funds and exchange-traded funds (ETFs). The law also strictly caps management fees. The goal is simple: force families into boring, steady, broad-market growth.

The Treasury Department launched the official Trump Accounts app nationwide to let parents manage everything directly from a phone. It handles recurring deposits and includes 15 financial literacy modules for parents and kids to review together. The app shows simple growth projections. For example, the official platform notes that if you leave a $1,000 seed deposit completely alone, it might reach $15,000 by adulthood. Toss in $250 a year, and it hits $51,000. Max out the full $5,000 annual limit, and the account could compound to a staggering $742,000 over time.

The Turn 18 Dilemma

Here is what most people get wrong about Trump Accounts: they aren't standard savings accounts. You cannot pull this money out when your teenager wants a car or needs summer camp tuition. Prior to age 18, withdrawals are completely banned, barring the death of the child.

When your child hits 18, the legal custody transfers entirely to them. They become the sole owner, and they face three choices:

- Keep it running: Leave the money exactly where it is.

- Rollover: Roll the balance into a Traditional IRA or convert it into a Roth IRA.

- Cash out: Liquidate the account.

If they decide to withdraw the cash at 18 to pay for a home, start a business, or handle higher education, the money gets taxed as ordinary income. Worse, if they use the funds for non-qualified expenses before age 59½, they face the standard 10% IRS early withdrawal penalty.

Trump Accounts vs 529 Plans

Don't abandon your existing college savings strategies just yet. A 529 plan remains far superior if your explicit goal is paying for tuition, housing, and textbooks, because 529 withdrawals for qualified education expenses are completely tax-free. Trump Account withdrawals are taxed as ordinary income.

However, Trump Accounts have a massive advantage if your child decides to skip college. Instead of dealing with the complex rollover rules of a 529, a Trump Account naturally pivots into a standard retirement vehicle. It provides a long-term foundation that standard savings accounts simply cannot match.

Next Steps for Parents

Don't leave free money on the table. If your child fits the criteria, follow these immediate steps:

- Verify eligibility: Ensure your child has a valid Social Security number and check if their birth year qualifies for the $1,000 Treasury deposit or the $250 location-based charitable deposit.

- File the paperwork: Log into your official account at IRS.gov or go straight to TrumpAccounts.gov to submit Form 4547 (the official election form). You'll need an ID.me account to complete it.

- Download the app: Grab the official Trump Accounts app from the iOS or Android store to monitor the validation status.

- Automate a baseline: Even if you can't hit the $5,000 annual cap, link your bank account and set a small monthly recurring transfer to capitalize on the power of compounding.